I recently built this dashboard for a discretionary market profile trader who was spending 30-45 minutes every morning piecing together the same information from four different sources: a premarket note, TradingView charts, an economic calendar website, and the options chain on their broker platform. The same ritual every day, and half of it was mechanical work that a script could do faster and more consistently.

The result is a single-page dashboard that generates automatically at 9:25 AM ET from live broker data. It pulls market profile, volume profile, gamma exposure, expected move, cash index context, and the economic calendar into one screen with four tabs. The trader opens one URL, scans for 15 seconds, and knows where price sits in context, what the options market implies about today’s range, and whether any events could move the tape. No chart setup, no tab switching, no manual calculations.

The dashboard is organized into four tabs. Here’s what each looks like with real data from May 12, 2026.

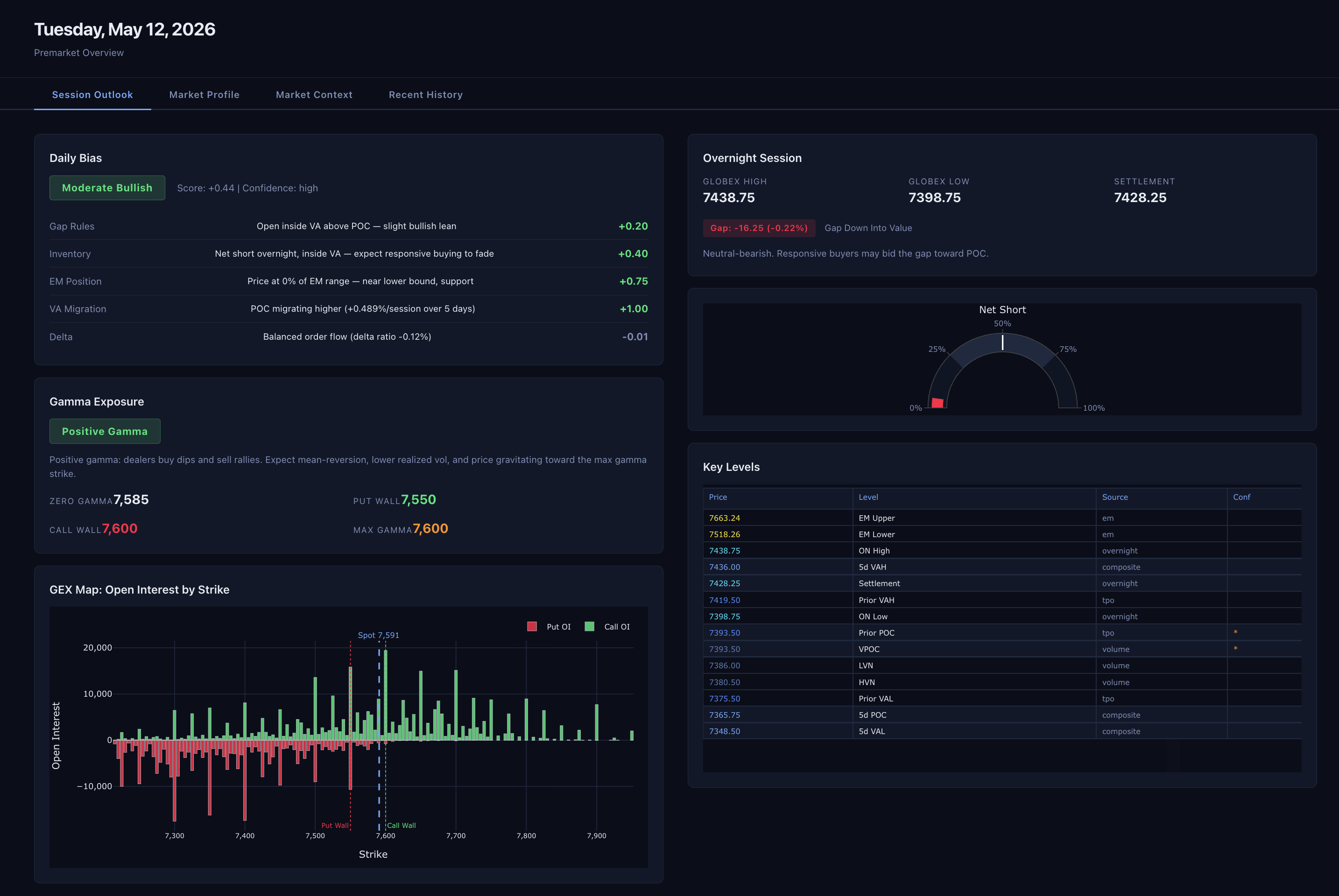

Session Outlook

The default view: daily bias scorecard, gamma exposure regime and GEX map, overnight session context, inventory positioning, and a synthesized key levels table.

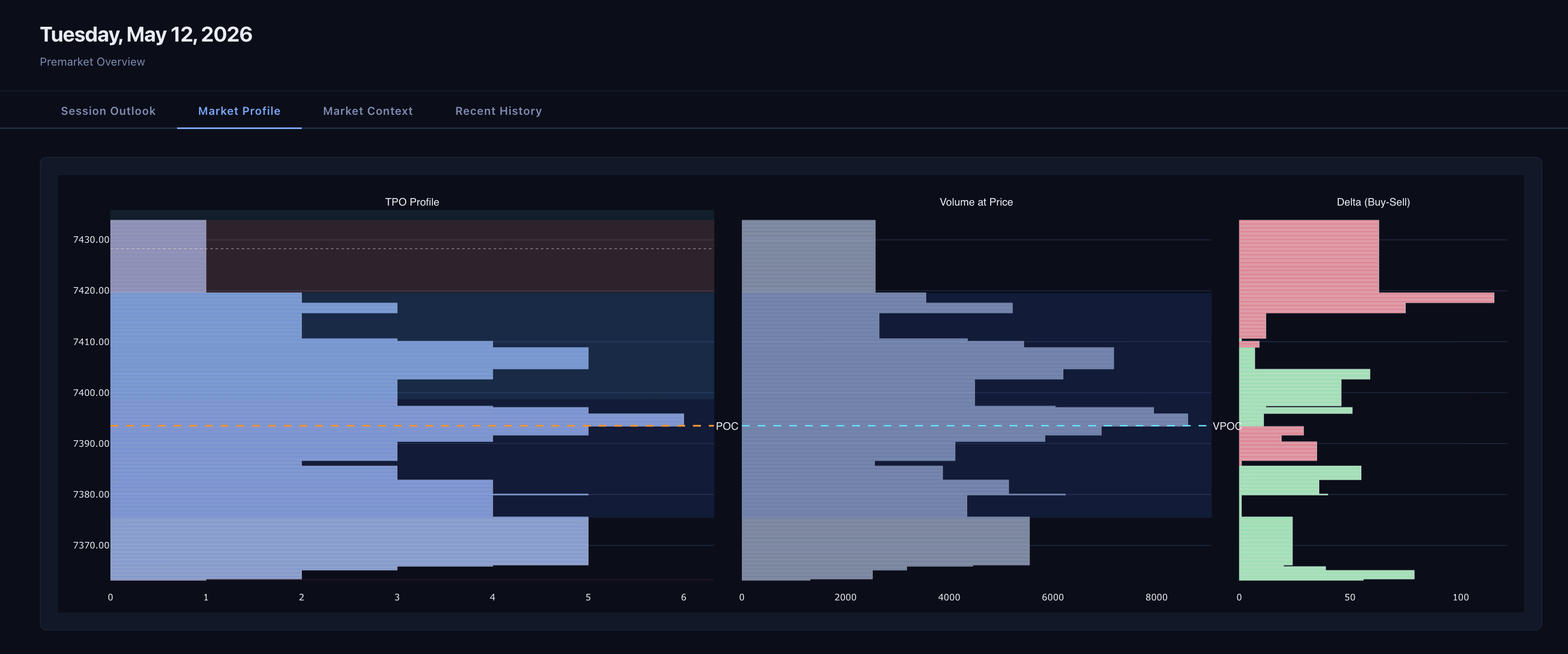

Market Profile

TPO profile, volume at price, and buy/sell delta side by side for the prior session.

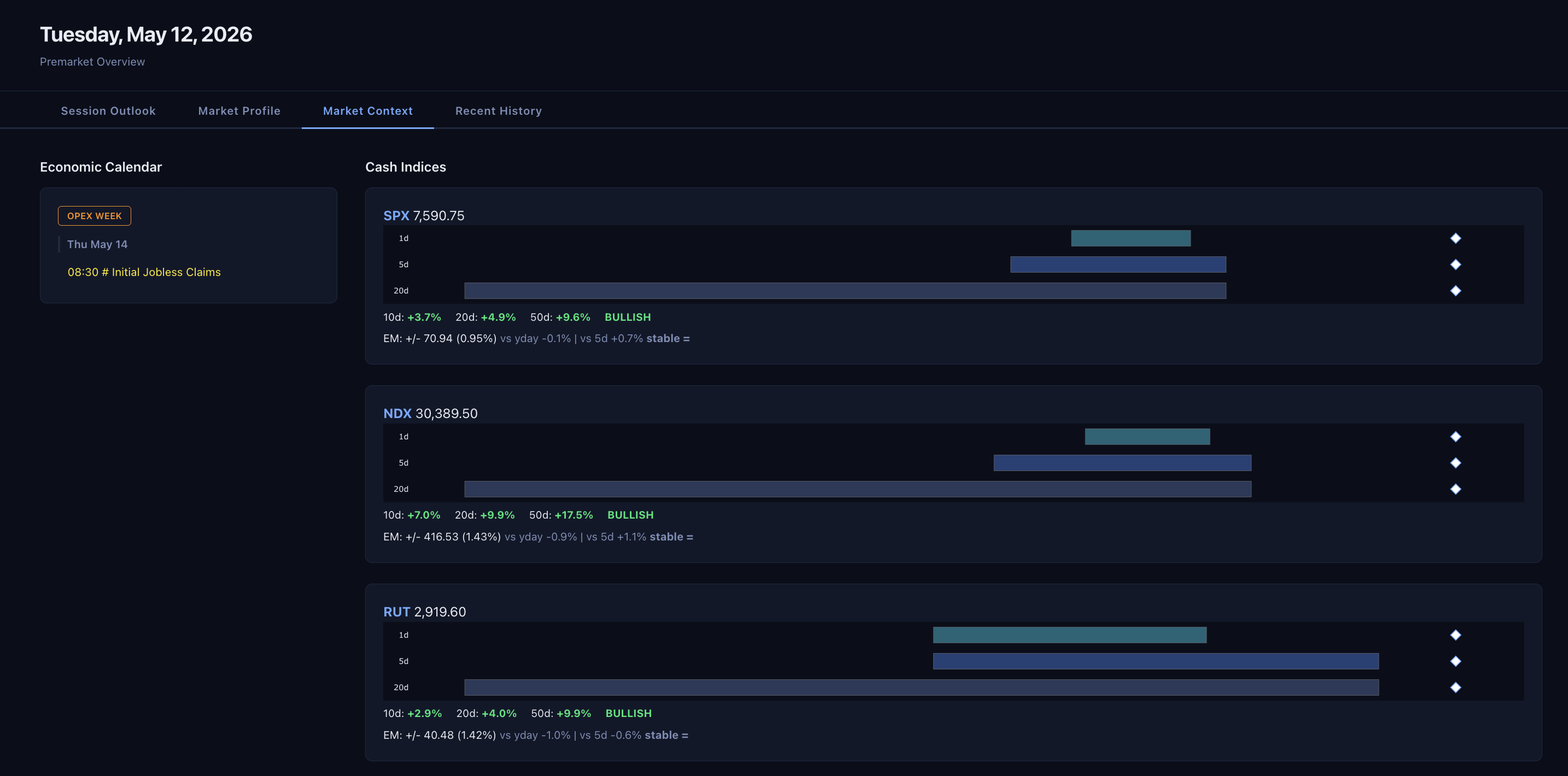

Market Context

Economic calendar (filtered to today, impact-ranked) alongside cash index context for SPX, NDX, and RUT: range positioning, moving average distances, trend alignment, and expected move with trend context.

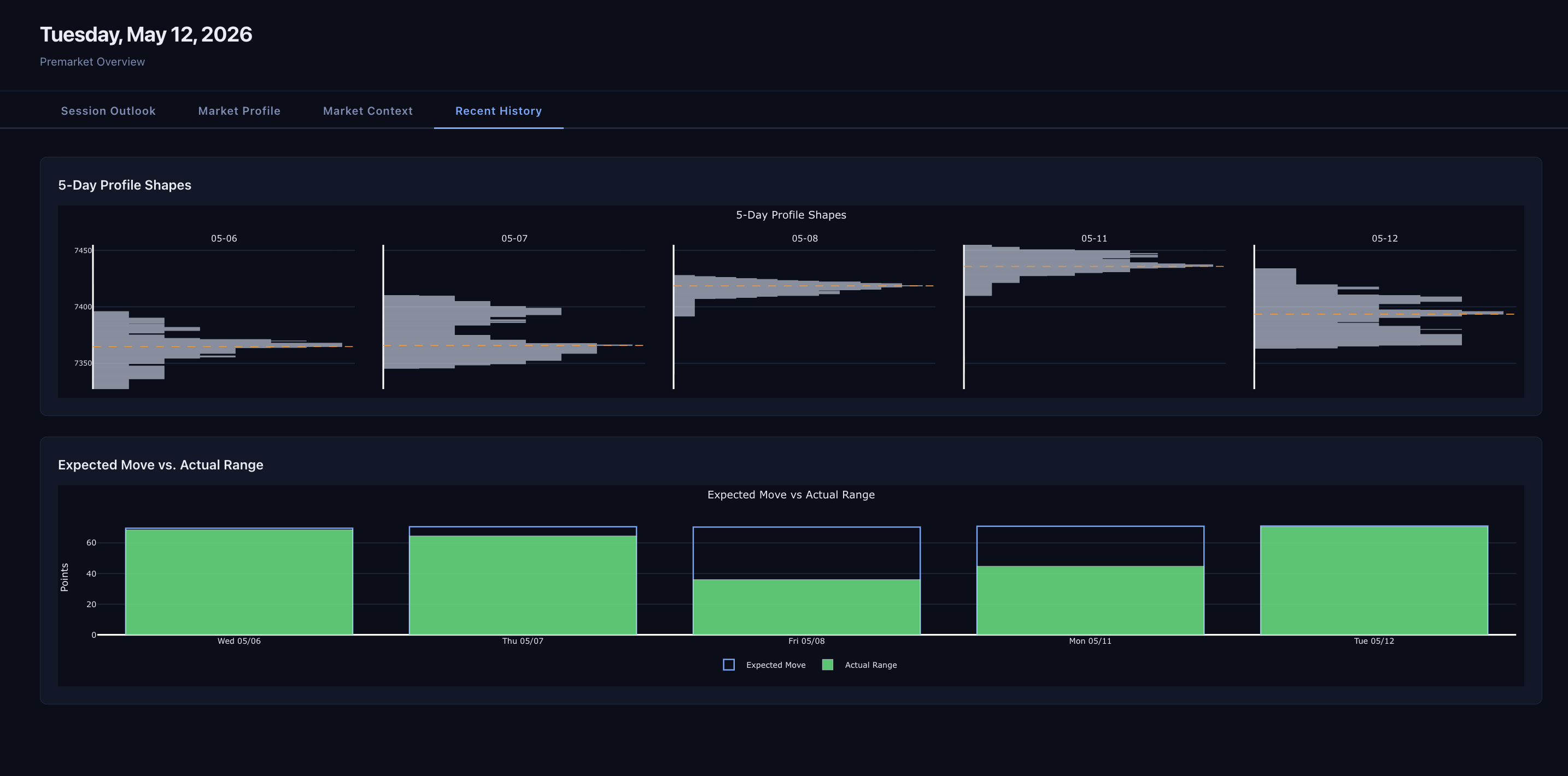

Recent History

Five-day profile shape comparison and expected move vs. actual range tracking to gauge whether the market is using or exceeding its implied range.

What follows is the design specification behind the dashboard: the data models, computation methods, panel layouts, and pipeline architecture. I’m sharing it because the thinking behind each panel is more useful than the code itself. If you trade market profile, you’ll recognize the concepts. If you build trading tools, you’ll see how the pieces fit together.

Design Specification

I. Dashboard Layout (Single Screen, 1400x1050)

+===================================================================+

| PREMARKET OVERVIEW Mon 2026-05-12 06:45 ET [ES][NQ][R] |

+===================================================================+

| | |

| A. CASH INDEX | C. MAIN INSTRUMENT |

| CONTEXT PANEL | TPO + VOLUME PROFILE |

| (SPX/NDX/RUT) | + OVERNIGHT OVERLAY |

| | + DELTA PROFILE |

| ~280px wide | |

| ~500px tall | ~780px wide, ~500px tall |

| | |

| - where in range | |

| - distance from MAs | |

| - expected move box | |

| - put/call ratio | |

| | |

+------------------------+------------------------------------------+

| | |

| B. ECONOMIC | D. KEY LEVELS E. 5-DAY |

| CALENDAR | + INVENTORY SPARKLINES |

| (today's events) | GAUGE + EXPECTED |

| | MOVE CONE |

| ~280px wide | ~480px wide ~300px wide |

| ~280px tall | ~280px tall ~280px tall |

| | |

+------------------------+------------------------------------------+

II. Panel A: Cash Index Context

Purpose

Give the trader an instant read on where each cash index sits relative to its own structure — not just the price, but the context around it. A swing trader needs to know: are we near the top of a range? How far from the mean? Is the market stretched or compressed?

Cash Index Data Sources

From TastyTrade DXLink Streamer:

Summaryevent forSPX,NDX,RUT:day_open_price,day_high_price,day_low_price,day_close_priceprev_day_close_price,prev_day_volume

Underlyingevent forSPX,NDX,RUT:volatility(30-day IV, VIX methodology)front_volatility,back_volatilityput_call_ratiocall_volume,put_volume,option_volume

- Historical

Candleevents (daily,"1d"interval) for 20-day lookback

From TradeStation REST API (backup/bulk history):

GET /v3/marketdata/barcharts/$SPX.Xwithunit=Daily,barsback=60- Same for

$NDX.Xand$RUT.X

Computations

1. Range Context (visual: bullet chart)

For each index, show where today’s price sits within multiple ranges:

@dataclass

class RangeContext:

price: Decimal

prior_day_high: Decimal

prior_day_low: Decimal

week_high: Decimal # 5-day high

week_low: Decimal # 5-day low

month_high: Decimal # 20-day high

month_low: Decimal # 20-day low

range_percentile: float # 0.0 = at 20d low, 1.0 = at 20d high

Visualization: nested bullet chart

SPX 5,892.40 [+0.34%]

20d |████████████████████●████| 78th %ile

5d |██████████████████████●██| 88th %ile

1d |█████████████●███████████| 55th %ile

Three thin horizontal bars stacked, each showing the price’s position within that time range. Instant visual read: “near the top of the weekly range but mid-range intraday.”

2. Distance from Key Moving Averages

@dataclass

class MAContext:

sma_10: Decimal

sma_20: Decimal

sma_50: Decimal

dist_from_10: float # percentage distance

dist_from_20: float

dist_from_50: float

trend_alignment: str # "bullish" (10>20>50), "bearish", "mixed"

Visualization: compact sparkline + distance labels A 60-day price sparkline (~120px wide) with the three MAs overlaid as colored lines. Below it, three compact distance readings:

10d: +0.4% 20d: +1.2% 50d: +3.8% [BULL]

Color-coded: green if price above MA, red if below.

3. Expected Move (see Section III for full computation)

A compact box showing:

┌─ EXPECTED MOVE (1d) ─────┐

│ SPX: +/- 42.3 (0.72%) │

│ vs yesterday: 38.1 │

│ vs 5d avg: 45.6 │

│ ▼ contracting │

└───────────────────────────┘

4. Put/Call Ratio Context

From the Underlying event:

P/C Ratio: 0.82 [5d avg: 0.91, 20d avg: 0.88]

Options Vol: 2.1M calls / 1.7M puts

A simple gauge:

BEARISH ←━━━━━━━━━━●━━━→ BULLISH

0.82

1.2 0.6

Combined Panel A Rendering

All four components stack vertically within ~280px width:

┌─ SPX 5,892.40 (+0.34%) ──────┐

│ │

│ [bullet chart: range context] │

│ [sparkline + MA distances] │

│ [expected move box] │

│ [P/C ratio gauge] │

│ │

├─ NDX 21,440 (+0.52%) ────────┤

│ [same four components] │

├─ RUT 2,105 (-0.12%) ─────────┤

│ [same four components] │

└────────────────────────────────┘

Each index gets ~160px of vertical space. The panel is dense but scannable — a trader can read the full cross-index context in 5 seconds.

III. Expected Move Computation

What It Is

The market’s implied 1-day price range, derived from at-the-money option prices. If the ATM straddle for tomorrow’s expiry costs $42, the market implies SPX will move roughly +/- $42 from the current price. This is the options market’s consensus forecast of magnitude (not direction).

Method 1: ATM Straddle Price (Most Direct)

The nearest-expiry ATM straddle mid price gives the market’s implied 1-day move directly. If the straddle costs $42, the market implies +/- $42. For multi-day expirations, scale by 1/sqrt(DTE) to get the 1-day equivalent.

@dataclass

class ExpectedMove:

magnitude: Decimal # absolute dollar move (1 sigma)

pct: float # as percentage of underlying price

upper: Decimal # underlying + magnitude

lower: Decimal # underlying - magnitude

source: str # "atm_straddle" or "implied_volatility"

dte: int = 1

Method 2: From Implied Volatility

Convert annualized IV to 1-day expected move: EM_1d = Price * IV * sqrt(1/252). This gives 1 standard deviation, roughly a 68% probability the actual move is smaller.

Comparison: Today vs. Yesterday vs. 5-Day Average

@dataclass

class ExpectedMoveContext:

today: ExpectedMove

yesterday: ExpectedMove

avg_5d: ExpectedMove

trend: str # "expanding", "contracting", "stable"

today_vs_yesterday: float

today_vs_5d_avg: float

The trend classification is simple: if today’s EM exceeds the 5-day average by more than 10%, volatility is expanding. Below 90%, contracting. Otherwise stable.

Visualization: Expected Move Cone (Panel E)

On the 5-day sparkline panel, overlay a translucent cone projecting from the current price:

Price

^

| ╱ today's EM

| ╱────────────

| ╱ ╱ 5d avg EM

| ╱───╱─────────────

| ●

| ╲───╲─────────────

| ╲ ╲

| ╲────────────

| ╲

+──────────────────────> Time

Prior 5 days Today

Two cones: the outer (lighter) is today’s EM, the inner (darker) is the 5-day average EM. If today’s cone is wider, volatility is expanding. The trader sees this at a glance without reading numbers.

IV. Panel B: Economic Calendar

Calendar Data Sources

Option 1: TradingEconomics API (preferred)

- Free tier: 1000 requests/month

- Endpoint:

GET /calendar?c=united-states&importance=3 - Fields:

Date,Event,Actual,Previous,Forecast,TEForecast,Importance - Importance: 1=low, 2=medium, 3=high

Option 2: Scrape CME FedWatch + FOMC calendar

- For rate decision probabilities specifically

Option 3: financialmodelingprep.com

GET /api/v3/economic_calendar?from=2026-05-12&to=2026-05-12- Fields:

event,date,country,actual,previous,estimate,impact

Option 4: Static calendar with known dates

For the most impactful events (FOMC, NFP, CPI, PPI, retail sales, GDP, jobless claims), the dates are published months in advance. A static calendar supplemented by API data is the most reliable approach.

@dataclass

class EconomicEvent:

time: time # ET

name: str

impact: str # "high", "medium", "low"

previous: str | None

forecast: str | None

actual: str | None # filled after release

@dataclass

class EconomicCalendar:

date: date

events: list[EconomicEvent]

fomc_day: bool

opex_week: bool # options expiration week

quarter_end: bool

### Known high-impact recurring events

HIGH_IMPACT_EVENTS = {

"FOMC Rate Decision",

"Nonfarm Payrolls",

"CPI (YoY)", "Core CPI (YoY)",

"PPI (YoY)", "Core PPI (YoY)",

"GDP (QoQ)",

"Initial Jobless Claims",

"Retail Sales (MoM)",

"PCE Price Index (YoY)",

"ISM Manufacturing PMI",

"ISM Services PMI",

"Consumer Confidence",

"Michigan Consumer Sentiment",

"JOLTS Job Openings",

"Durable Goods Orders",

}

What Makes an Event “Market Moving” for a Day Trader

Not all economic events matter equally. The dashboard should filter and rank by likely intraday impact:

Tier 1 — high probability of moving ES 10+ points:

- FOMC rate decisions and statements

- Nonfarm payrolls (first Friday of month)

- CPI / Core CPI (typically mid-month)

- Major geopolitical events (can’t predict, but flag if known)

Tier 2 — moderate probability of moving ES 5-10 points:

- PPI, retail sales, GDP revisions

- Initial jobless claims (every Thursday 8:30 ET)

- ISM Manufacturing and Services PMI

Tier 3 — usually low impact but can surprise:

- Consumer confidence, Michigan sentiment

- Housing data, durable goods

- Fed speakers (impact depends on who and timing)

Visualization

A compact timeline with only today’s events, color-coded by impact:

┌─ CALENDAR Mon 2026-05-12 ───────────────────┐

│ │

│ 08:30 ██ CPI (YoY) Est: 2.4% Prev: 2.6% │

│ 08:30 ██ Core CPI (YoY) Est: 2.8% Prev: 2.8% │

│ 10:00 █ Michigan Sent. Est: 67.5 Prev: 65.2 │

│ 13:00 10Y Auction │

│ 14:00 Fed Barkin speaks │

│ │

│ ██ = high impact █ = medium (blank) = low │

│ │

│ Flags: OPEX WEEK │

└───────────────────────────────────────────────┘

Events are sorted by time. Pre-market events (before 9:30) are separated from intraday events. The forecast vs. previous is shown inline so the trader knows what the market expects.

After the release, Actual replaces Est: and is colored green (better

than expected) or red (worse). This is a live update if the dashboard

is served as a web page.

Contextual Flags

Beyond individual events, flag structural calendar conditions:

def compute_calendar_flags(cal_date: date) -> list[str]:

flags = []

# OPEX week (third Friday of month)

if is_opex_week(cal_date):

flags.append("OPEX WEEK")

# Quad witching (third Friday of Mar/Jun/Sep/Dec)

if is_quad_witching(cal_date):

flags.append("QUAD WITCHING")

# Month-end rebalance window (last 3 trading days)

if is_month_end_window(cal_date):

flags.append("MONTH-END REBAL")

# FOMC blackout period

if is_fomc_blackout(cal_date):

flags.append("FOMC BLACKOUT")

# First/last day of quarter

if is_quarter_boundary(cal_date):

flags.append("QUARTER BOUNDARY")

# VIX expiration (typically Wed before 3rd Fri)

if is_vix_expiration(cal_date):

flags.append("VIX EXP")

return flags

These structural events affect market behavior in predictable ways:

- OPEX week: increased gamma exposure, potential pinning effects

- Month-end: pension and index fund rebalancing flows

- FOMC: reduced liquidity in lead-up, volatility spike on release

- Quad witching: massive volume, unusual price action at close

V. Panel C: Main TPO + Volume Profile (Expanded)

This is the same centerpiece panel from the prior design, but with two additions:

Addition 1: Delta Profile (from TastyTrade bid_volume/ask_volume)

A third column alongside the TPO and volume profiles:

Price TPO Profile Volume Profile Delta Profile

5895 BBB ████ ██▓ (+)

5894 BBCC ██████ ████▓ (+)

5893 ABCCD █████████ ←VPOC ░░░░░ (neutral)

5892 AABCCCDD ████████████ ░░░░░░░ (-)

5891 AABCD ←POC ██████████ ░░░░░░░░░ (-)

5890 AABCD ████████ ░░░░░░ (-)

5889 AAB ████ ░░░░ (-)

Delta = bid_volume - ask_volume at each price level.

- Positive delta (green): more aggressive buying (lifting offers)

- Negative delta (red): more aggressive selling (hitting bids)

- This shows WHERE buyers and sellers were active, not just how much volume traded. A high-volume node with negative delta is distribution (selling into strength). One with positive delta is accumulation.

def compute_delta_profile(candles_by_price: dict[Decimal, list[Candle]]):

"""Compute cumulative delta at each price level."""

delta_at_price = {}

for price, candles in candles_by_price.items():

bid_vol = sum(c.bid_volume or 0 for c in candles)

ask_vol = sum(c.ask_volume or 0 for c in candles)

delta_at_price[price] = bid_vol - ask_vol

return delta_at_price

Addition 2: Expected Move Bounds on the Price Axis

Draw two horizontal dashed lines on the TPO panel at:

current_price + expected_move(upper EM bound)current_price - expected_move(lower EM bound)

This shows the trader where the options market expects price to stay today, overlaid directly on the structural levels from the profile. If the upper EM bound aligns with a volume node or value area edge, that level becomes doubly significant.

VI. Panel D: Key Levels Table + Inventory Gauge (Expanded)

Level Synthesis

Merge levels from all sources and rank by significance:

@dataclass

class Level:

price: Decimal

label: str

source: str # "tpo", "volume", "overnight", "cash", "em", "ma"

significance: int # 1-5, 5 = most significant

confluence: int # how many sources agree within N ticks

def synthesize_levels(

tpo_profile: MarketProfile,

vol_profile: VolumeProfile,

overnight: OvernightAnalysis,

composite: CompositeProfile,

cash_context: dict[str, RangeContext],

expected_move: ExpectedMove,

ma_context: MAContext,

) -> list[Level]:

"""Merge all levels, detect confluence, rank by significance."""

raw_levels = []

# TPO levels

raw_levels.append(Level(tpo_profile.poc, "Prior POC", "tpo", 4, 0))

raw_levels.append(Level(tpo_profile.vah, "Prior VAH", "tpo", 3, 0))

raw_levels.append(Level(tpo_profile.val, "Prior VAL", "tpo", 3, 0))

# Volume profile levels

raw_levels.append(Level(vol_profile.vpoc, "VPOC", "volume", 4, 0))

for hvn in vol_profile.hvns:

raw_levels.append(Level(hvn, "HVN", "volume", 2, 0))

for lvn in vol_profile.lvns:

raw_levels.append(Level(lvn, "LVN", "volume", 2, 0))

# Overnight

raw_levels.append(Level(overnight.globex_high, "ON High", "overnight", 3, 0))

raw_levels.append(Level(overnight.globex_low, "ON Low", "overnight", 3, 0))

raw_levels.append(Level(overnight.settlement, "Settlement", "overnight", 4, 0))

# Composite

raw_levels.append(Level(composite.poc, f"{composite.n_days}d POC", "tpo", 5, 0))

raw_levels.append(Level(composite.vah, f"{composite.n_days}d VAH", "tpo", 4, 0))

raw_levels.append(Level(composite.val, f"{composite.n_days}d VAL", "tpo", 4, 0))

# Expected move bounds

raw_levels.append(Level(expected_move.upper, "EM Upper", "em", 2, 0))

raw_levels.append(Level(expected_move.lower, "EM Lower", "em", 2, 0))

# Moving averages (mapped to futures via basis adjustment)

# ...

# Detect confluence: levels within 2 points of each other

for i, level in enumerate(raw_levels):

for j, other in enumerate(raw_levels):

if i != j and abs(level.price - other.price) <= 2:

raw_levels[i] = replace(level, confluence=level.confluence + 1)

# Boost significance for confluent levels

for level in raw_levels:

if level.confluence >= 2:

level.significance = min(5, level.significance + 1)

return sorted(raw_levels, key=lambda l: l.price, reverse=True)

Visualization: Levels Table with Confluence Markers

Price Level Source Conf │ ← ON Range →

─────────────────────────────────────────│──────────────

5,895 EM Upper Options · │ ·

5,892 ON High Overnight ·· │ ●

5,889 5d VAH Composite ··· │ ●

5,885 Prior VAH TPO · │ ●

5,881 VPOC / Prior Vol+TPO ···· │ ● ← CONFLUENT

5,878 Settlement Session · │ ●

5,871 Prior VAL TPO · │●

5,865 5d VAL Composite ·· │●

5,860 ON Low Overnight · │●

5,855 EM Lower Options · │·

The dot-plot column on the right shows spatial relationships. Confluence dots (····) tell the trader which levels have multiple structural reasons to matter.

VII. Panel E: 5-Day Sparklines + Expected Move Cone

5-Day Profile Sparklines

Five tiny TPO profile silhouettes (no labels, just shapes) showing the profile evolution:

Mon Tue Wed Thu Fri

╻ ╻╻ ╻ ╻╻╻ ╻╻

╻╻ ╻╻╻ ╻╻ ╻╻╻╻ ╻╻╻

╻╻╻ ╻╻╻╻ ╻╻╻ ╻╻╻╻╻ ╻╻╻╻ ← widening = balance

╻╻╻╻ ╻╻╻ ╻╻╻╻ ╻╻╻╻ ╻╻╻╻╻

╻╻╻ ╻╻ ╻╻╻ ╻╻╻ ╻╻╻╻

╻╻ ╻ ╻╻ ╻╻ ╻╻╻

╻ ╻ ╻ ╻╻

Overlaid annotations:

- A horizontal line connecting each day’s POC shows value migration

- Value area high/low connected across days shows balance/expansion

- Today’s expected move cone extends from Friday’s close

Expected Move Comparison Strip

Below the sparklines, a compact strip comparing today’s EM to recent:

EM History (1-sigma, points)

Mon ████████████████████░░░░ 42.3

Tue █████████████████░░░░░░░ 38.1

Wed ██████████████████████░░ 46.2

Thu ████████████████████████ 48.9 ← vol spike (CPI day)

Fri ███████████████████░░░░░ 40.5

─────────────────────────────────────

Today █████████████████████░░░ 44.1 5d avg: 43.2

Filled bars = actual range that day. Unfilled = EM that wasn’t used. This shows whether the market is using its full expected move or trading inside it. Consistently using >100% of EM suggests the IV model underestimates realized vol. Consistently using <70% suggests the options are overpriced (useful for options sellers).

VIII. Actual Range vs. Expected Move Tracking

This is an analytical edge that most premarket services don’t offer.

@dataclass

class RangeVsEM:

date: date

expected_move: Decimal # 1-sigma EM at open

actual_range: Decimal # high - low for the session

range_em_ratio: float # actual_range / expected_move

settled_within_em: bool # did price close within EM bounds?

The computation is straightforward: range_em_ratio = (high - low) / expected_move for each session.

Why this matters for traders:

- If the market has been using only 60% of its EM for 5 straight days, it’s “coiling” — volatility compression often precedes expansion

- If the market exceeded 100% of EM 3 of the last 5 days, realized vol is running ahead of implied vol — expect options premiums to catch up

- The ratio trend (expanding or contracting) tells you whether the market is becoming more or less predictable

IX. Data Pipeline Architecture

┌──────────────┐

│ TastyTrade │

│ DXLink │

│ Streamer │

└──────┬───────┘

│ Candle (1m, 30m)

│ Quote, Summary

│ Underlying (IV, P/C)

│ Greeks (for EM calc)

▼

┌──────────────┐ ┌──────────────┐ ┌──────────────┐

│ TradeStation │ │ │ │ Economic │

│ REST API │───▶│ QuestDB │◀───│ Calendar API │

│ (bulk hist) │ │ (storage) │ │ (or static) │

└──────────────┘ └──────┬───────┘ └──────────────┘

│

▼

┌──────────────┐

│ Polars │

│ (compute │

│ profiles, │

│ EM, etc.) │

└──────┬───────┘

│

┌──────┴───────┐

▼ ▼

┌───────────┐ ┌───────────┐

│ matplotlib │ │ Jinja2 │

│ (SVG/PNG) │ │ (Hugo .md)│

└─────┬──────┘ └─────┬─────┘

│ │

▼ ▼

┌───────────────────────────┐

│ Hugo site / daily post │

│ content/premarket/ │

│ 2026-05-12.md │

└───────────────────────────┘

Data Fetch

A single fetch at ~09:25 ET captures everything needed: prior session daily bars (20-day lookback), the finalized overnight range, the economic calendar for the day, and current IV for expected move computation. Compute all profiles and render the dashboard immediately after. The entire pipeline runs once, produces one snapshot, and is done before the 09:30 open.

Futures Symbol Resolution

Futures symbols follow the standard month code convention (H=Mar, M=Jun, U=Sep, Z=Dec for quarterly contracts). The dashboard needs to resolve the front-month contract automatically based on the current date and the quarterly expiration cycle.

The cash-to-futures basis (futures price minus cash index price) is needed to map cash index levels (like SPX moving averages) onto the futures price axis in the TPO panel.

X. What This Dashboard Replaces

The trader I built this for was doing all of this manually every morning:

| What they were doing | How long it took | What the dashboard does instead |

|---|---|---|

| Reading a premarket note (~2800 words) | 5-8 min | 15-second scan of the Session Outlook tab |

| Setting up TradingView charts per instrument | Several minutes of clicking | All 3 instruments, profiles auto-computed |

| Checking an economic calendar website | Separate tab, filtering by country | Pre-filtered to today, impact-ranked |

| Digging through broker options chain for expected move | Navigation through multiple screens | Front and center with trend context |

| Calculating MA distance with a ruler on the chart | Per instrument, per MA | All indices, all MAs, at a glance |

The total went from 30-45 minutes of prep to opening one URL and scanning for 15 seconds. The dashboard doesn’t replace their trading judgment. It replaces the mechanical work of assembling the context they need to apply that judgment.

Interested?

I built this for one trader’s workflow, but the problems it solves are common to anyone who trades market profile on index futures. If you’re a market profile trader spending your mornings assembling the same context from multiple sources, I’d be interested in hearing whether a tool like this would be useful to you. Reach me at me@susanpotter.net .

Susan Potter

Quant

Work with me

I spent the first half of my career building risk models and market data infrastructure at BNP Paribas, Bank of America, and Citadel, then fourteen years shipping production systems at scale. Now I bring both sides to quantitative trading. If you're a trading firm, family office, or fund looking to tighten the connection between your research ideas and your production trading systems, whether that's building validation pipelines, formalizing signal logic, or getting microstructure analytics into a deployable state, I'd like to hear what you're working on. Reach me at me@susanpotter.net.